Did tax fraud and the shadow economy decline in the aftermath of the pandemic? Analysis 2019-23 based on VAT collection.

Francisco de la Torre

21 Mar, 2024

In 2020, the fall in tax revenues exceeded the fall in GDP, with a probable growth of the underground economy in tandem with the decline in economic activity. In contrast, the growth in tax revenue between 2021 and 2023 exceeded forecasts, reaching above pre-pandemic levels.

To explain this unexpected growth, this study considers the emergence of the underground economy as a possible mechanism. To do so, this policy brief looks at whether there is higher VAT collection as a sign of surfacing, adapting the EVADE (Evaluating Value Added Duty Economy) methodology to statistics from the State Tax Administration Agency and the National Institute of Statistics.

Our findings:

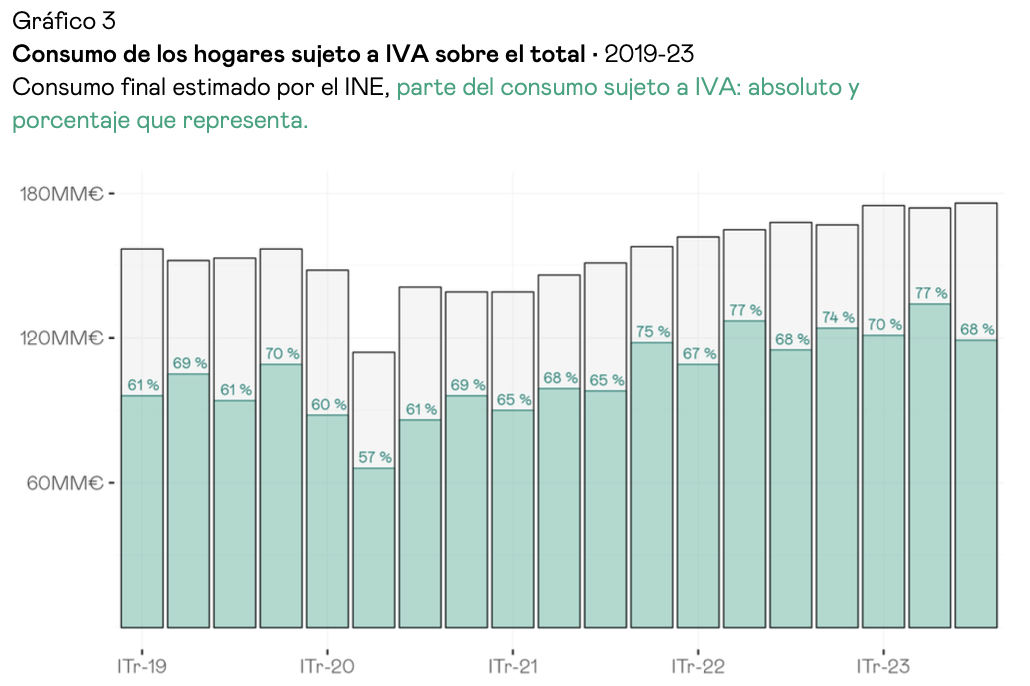

- The percentage of household consumption that pays VAT grew between six and seven points without significant changes in regulations, something that can only be explained by outcropping.

- This increase in the bases subject to control led to an increase in VAT revenue of around 6 billion euros per year in both 2022 and 2023.

To explain what may have caused this improved compliance, we hypothesize that during the pandemic there would have been social changes (possibly also stemming, at least in part, from the anti-fraud regulations) that led to an increase in card payments, decreasing the percentage of cash transactions, which are not equally controlled by the Tax Agency.

To explore this hypothesis, we analyze the Bank of Spain’s small transactions data for this period (2019-2023), distinguishing between card sales payments and ATM cash withdrawals.

- Indeed, we observe that the percentage of consumption paid by credit card, which is subject to greater control than cash, increased significantly.

- In addition, cash withdrawals barely grew in the same period, despite inflation.

To consolidate these good results, we recommend:

- Introduce more measures to encourage controlled payments.

- Extend and deepen the collection and exploitation of information to improve voluntary tax compliance, thus reducing tax fraud and the underground economy.

Related content